Understand how the EU's initiatives for sustainability are connected

Sustainability is a complex area, especially when new EU legislation, abbreviations and acronyms are included in the equation. To understand how sustainability through legislation becomes an integral part of the reality of modern businesses, it is necessary to delve into the EU's many directives and regulations, such as the CSRD (Corporate Sustainability Reporting Directive).

The EU's requirements have become more concrete and measurable. The wording of the legislation is precise, and tools are being developed that make it easier to measure CO2 emissions. Standards such as ESRS (European Sustainability Reporting Standards) offer companies better conditions for acting sustainably.

In this section, we will explore the connection between key concepts such as ESG (Environmental, Social, Governance), CSRD, DPP (Digital Product Passport) and ESRS. These are all key elements of the new wave of legislation that the EU is currently implementing.

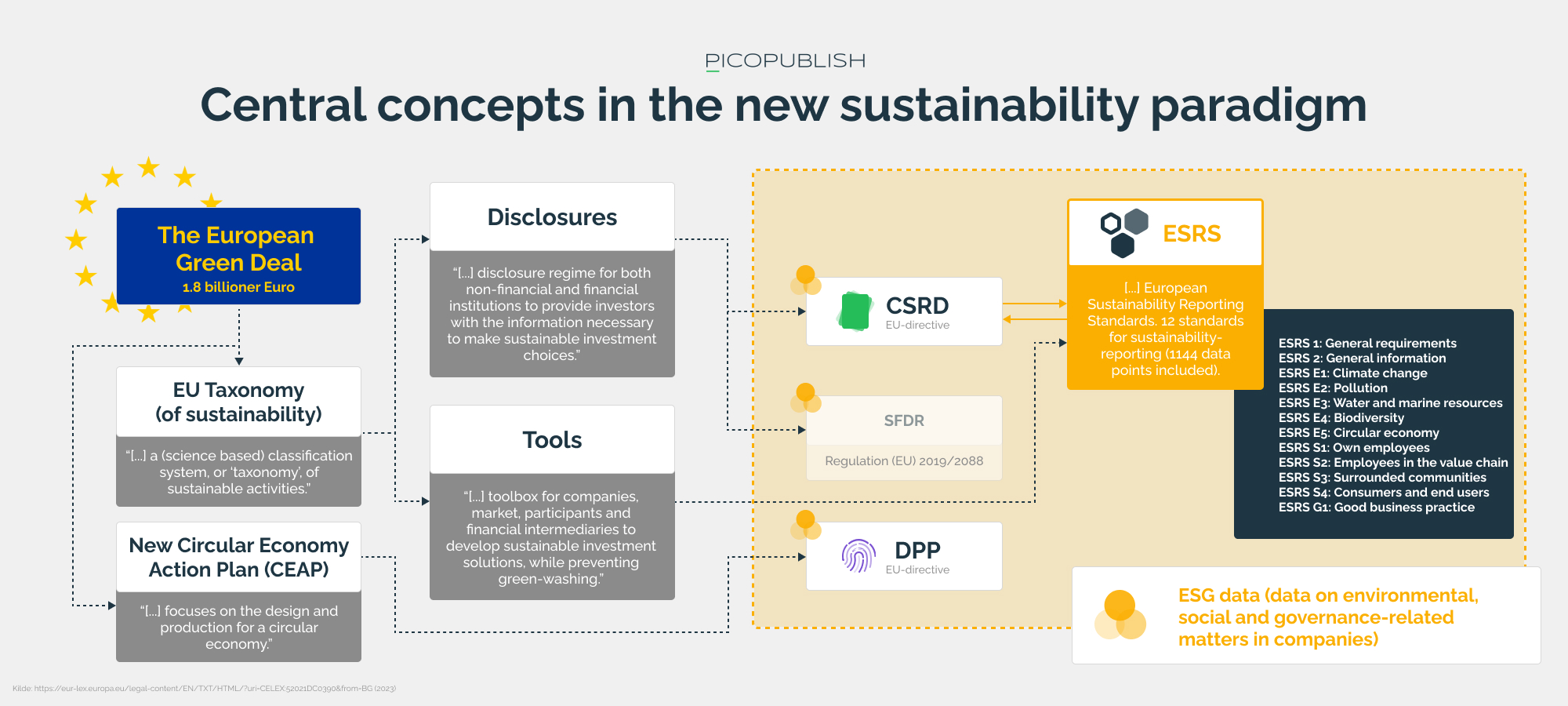

The EU's Green Deal has a budget of approx. 600 billion euros, which by 2050 will help ensure that the EU becomes climate neutral ("zero net emission").

The European Green Deal - where it all starts

The EU's focus on tackling the climate challenges facing the world has led to the development of The European Green Deal. The agreement includes that the EU plans to allocate 600 billion from the NextGenerationEU-pool to support a number of sustainability initiatives.

Objective; a climate-neutral EU by 2050.

The overall goal is to make the EU climate neutral by 2050. To achieve this goal, the EU will launch a number of initiatives in the coming years to promote the green transition through directives and regulations. In other words, it means that the EU is preparing new climate legislation that Member States must comply with.

In practice, sustainability will in the future be a matter of compliance with the law. New requirements for reporting sustainability data will be implemented through this new legislation - either at EU level or directly within member states' own national legal systems.

*out of a total budget of 1.8 trillion.

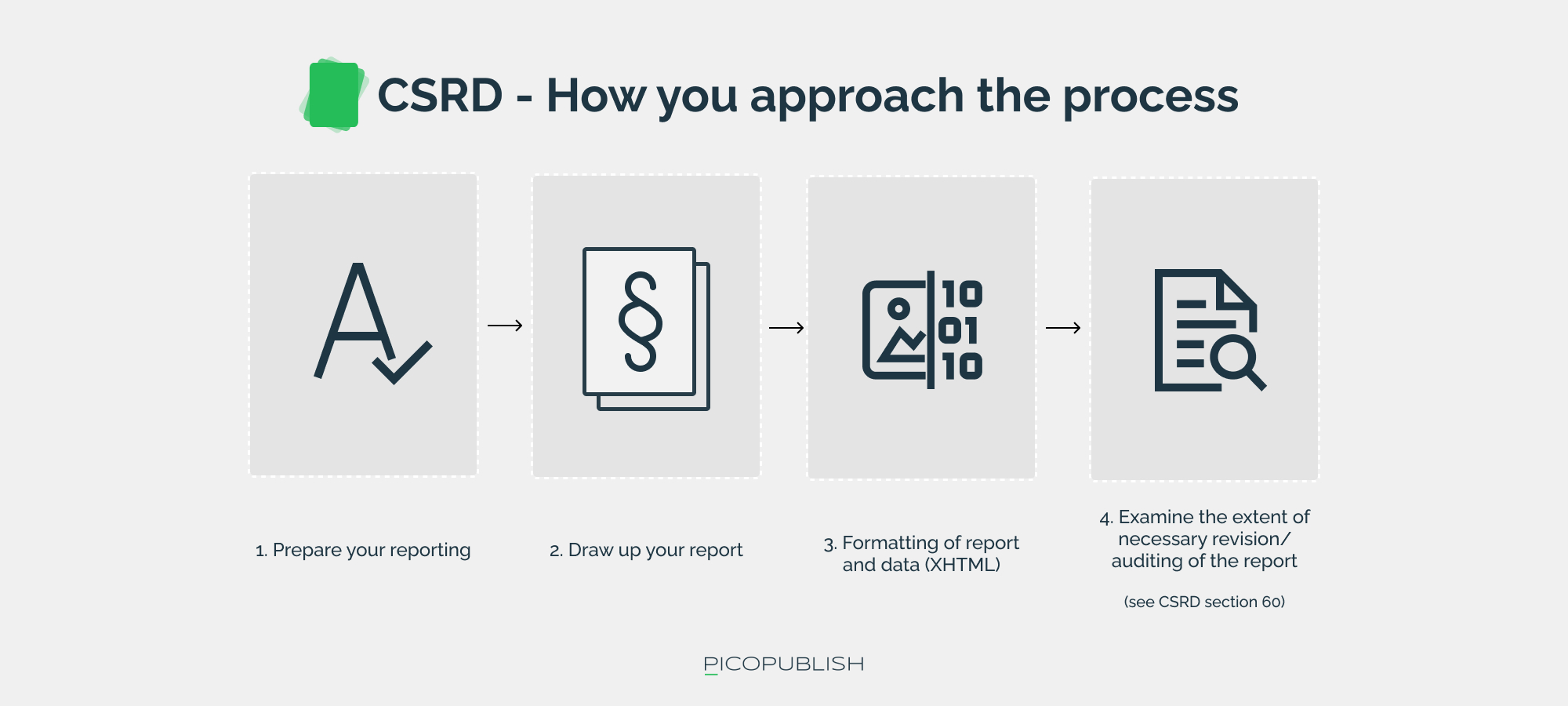

CSRD and sustainability reporting - applicable by law from the financial year 2024!

The most current example of sustainability legislation from the EU is the Corporate Sustainability Reporting Directive (CSRD). The CSRD Directive is particularly relevant for two reasons:

- The CSRD has broad coverage, as it applies to all companies with 500+ employees and listed companies, without distinguishing between industries.

- The CSRD requires reporting as of the 2024 financial year, which is now.

The CSRD means that companies must provide comprehensive reporting and documentation of their social and environmental impacts on society in the future.

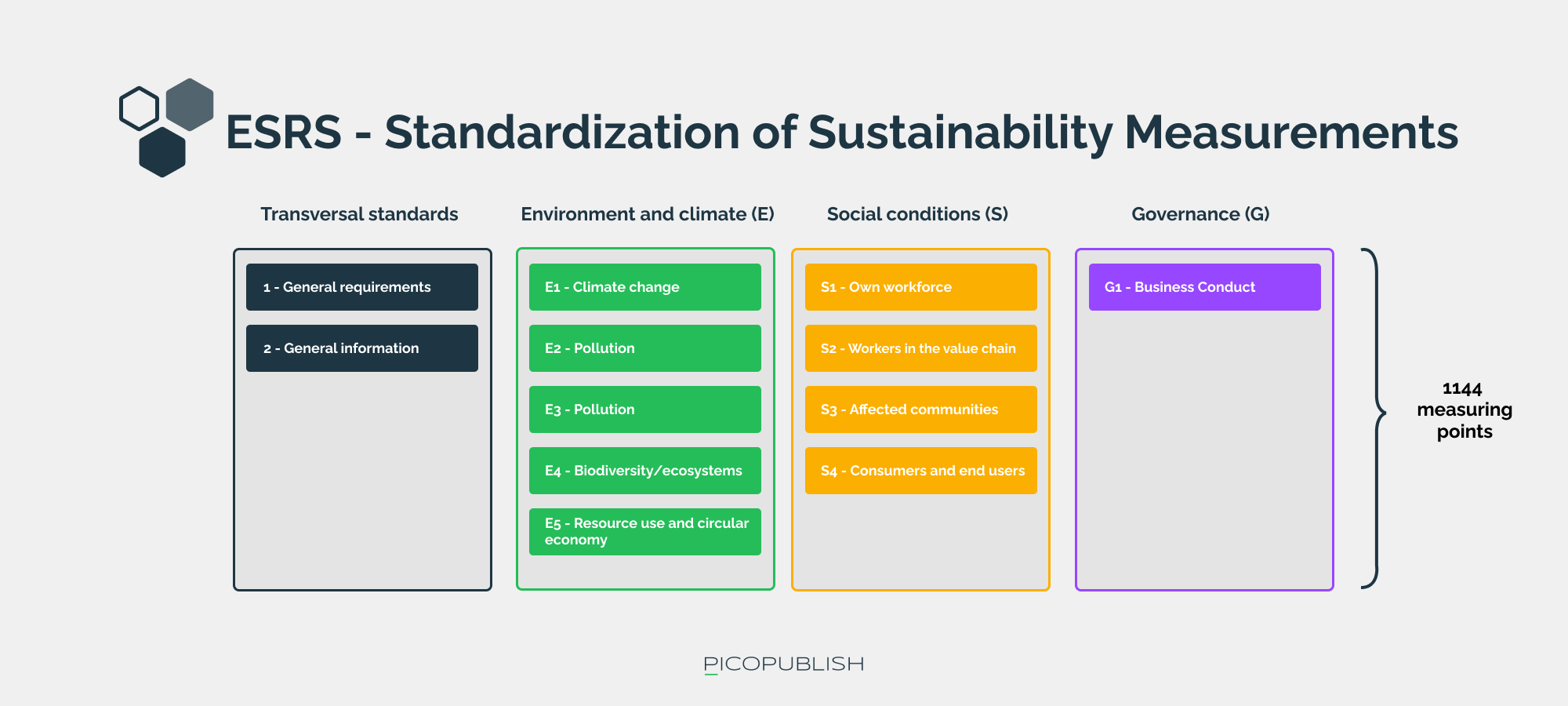

ESRS standard: 1144 metrics for CSRD reporting

Based on the ESRS reporting framework, which entered into force on 1 January 2024, companies covered by the CSRD Directive must report how they affect the environment and the surrounding society in the value chains they are part of.

The reporting must follow a "double materiality principle". This principle implies that companies are held accountable for the extent to which they take into account their own impact on social, political and environmental conditions that they believe influence their actions in the market.

An interesting detail about CSRD is that it is up to each company to choose which parameters they want to report on, which means that no company has to report on all 1144 parameters.

CSRD also affects small businesses!

Regardless of whether a company is directly or indirectly covered by the requirements of the Directive, most companies will probably have to relate to the content of the Directive. As often seen before, larger companies will try to involve their partners in meeting the sustainability reporting requirements associated with the CSRD.

Smaller companies should therefore prepare to provide sustainability data to their business partners who are directly covered by the Directive.

As the CSRD is an EU directive, the content of the directive will be implemented in the national legislation of the member states. In Denmark, for example, the CSRD will be legally enforced from 1 July 2024.

Want to talk data?

If you’re interested in hearing our ideas on how data can help your business execute, grow, and scale, we’re ready for a no-obligation conversation.

How does CSRD relate to the other concepts?

The reports that companies will prepare in the future as a direct consequence of the introduction of the CSRD Directive will contain ESG data. This includes data on the company's environmental, social and governance activities.

CSRD and ESG: Sustainability Data Reporting

The ESRS standard's section E1 ("Climate Change") highlights as an example:

"[...] an explanation of the decarbonisation levers identified, and key actions planned, including changes in the undertaking's product and service portfolio and the adoption of new technologies in its own operations, or the upstream and/or downstream value chain" (Source: EFRAG).

This requires companies to take a stand on how their products and services are manufactured and what CO2 footprint production and sales have - both upstream and downstream.

The relationship between the CSRD and ESRS

CSRD reporting is based on the ESRS standard, which contains 14 categories and 1144 measurement points. To a greater or lesser extent, companies must take a position on these points in their reporting. A Product Information Management (PIM) system can be useful for storing and structuring data related to the products a company buys and sells, as well as for facilitating the preparation of the report.

The interaction between CSRD and DPP

The DPP (the EU's upcoming Digital Product Passport) is a separate EU initiative that aims to create a digital sustainability passport for products that contains information about their CO2 footprint, recyclability, etc. Although there is no direct coincidence between the CSRD and the DPP, the Digital Product Passport can serve as an integral part of CSRD reporting. This can give companies an opportunity to "kill two birds with one stone" by using data from the Digital Product Passport directly in their sustainability reporting.

ESG – A Unifying Term for Sustainability Data in a New EU Paradigm

ESG is an umbrella term for issues and data related to the areas of "Environmental," "Social," and "Governance."

The term "ESG" serves as a broad concept for sustainability data, making it a likely fixture in the language we use as we discuss the green transition and sustainability moving forward.

Although the origins of the term might seem unclear, it is widely recognized that the ESG concept gained prominence with the World Bank's 2004 report, "Who Cares Wins." This report, which focused on the green transition, introduced ESG data right from the beginning, highlighting its significance.

As the world moves towards a more sustainable future, those engaged in green transition and sustainability will undoubtedly encounter the ESG concept. It is expected to become the collective term for various activities, courses, certifications, and services related to sustainability reporting, such as those within the framework of the CSRD directive.

How does ESG relate to the other concepts?

ESG represents the most far-reaching concept among those we have mentioned. Almost all data related to sustainability reporting falls into the social, environmental or corporate (governance) categories;

- When a company reports on their whistleblower scheme in connection with their CSRD report, this falls under the governance-aspect.

- When a company shares their goal of reducing energy consumption in their CSRD report, they address environmental concerns.

This shows how the ESG concept works as an integrated framework for sustainability reporting, where each component - be it environmental, social or governance - plays a significant role in shaping companies' contribution to a more sustainable future.

ESRS - standardization of sustainability reporting

Much has been said about the green transition, which for many years has been a central topic in companies' CSR profiling. However, "exactly" is rarely a word associated with this discourse.

In recent years, concepts such as "greenwashing" have become an essential part of the debate. In 2022, a verdict was handed down in a case where a company was convicted of marketing PVC-enriched products as "environmentally friendly".

Sustainability standards and CSRD

To make sustainability reporting more accurate and quantifiable, the EU has developed the ESRS standard in collaboration with EFRAG, which forms the foundation for CSRD reporting.

EFRAG (European Financial Reporting Advisory Group) assists the EU in the development of legislation and standards for financial reporting. With ESRS (European Sustainability Reporting Standards), EFRAG has created a comprehensive reporting template consisting of 1144 points that serve as the basis for companies' CSRD reporting.

Reporting of "essential" parameters

Companies are required to carry out a double materiality assessment to determine the relevance of different social, environmental or societal factors for reporting. This double materiality principle ensures that companies consider both their impact on and their impact on ESG parameters.

In doing so, companies are encouraged to put themselves in an ethical and moral mirror when reporting on matters that affect staff, the environment, employment conditions and general trends in the local community.

The ESRS standard: a comprehensive reporting framework

The ESRS standard includes 12 categories:

- General principles

- General disclosures

- Climate Change

- Pollution

- Water & marine resources

- Biodiversity & ecosystems

- Resource use and circular economy

- Own workforce

- Workers in the value chain

- Affected communities

- Consumers and end-users

- Business conduct

These categories reflect the breadth of sustainability reporting. Both large and small companies need to prepare for the fact that data on these areas will soon become a crucial factor in their trade relations.

Companies with the necessary data become attractive trading partners, while those without data risk being excluded from supply chains where electronic data interchange (EDI) becomes a prerequisite for cooperation.

How does ESRS relate to the other concepts?

ESRS (European Sustainability Reporting Standards) have been prepared by EFRAG, which is a private, EU-supported consultancy company that prepares guidelines for financial reporting in Europe.

How ESRS and CSRD are linked - the underlying reporting standard

In short, the CSRD report must be based on the ESRS standard. The ESRS standard contains 14 categories and 1144 measurement points that companies must consider to a greater or lesser extent when preparing their ESG reports.

How ESRS and DPP are connected - the underlying reporting standard

What DPP and ESRS have in common is that they are both tools for measuring and reporting ESG data.

The DPP concept is still so new that we do not yet know what requirements will be placed on the companies.

However, it is special for DPP that we are talking about product-related data. In this context, the PIM system stands out as an obvious candidate for collecting, organizing and publishing the necessary data. We have written an article about this here - "Why is the EU's upcoming "Digital Product Passport" interesting for PIM system owners?".

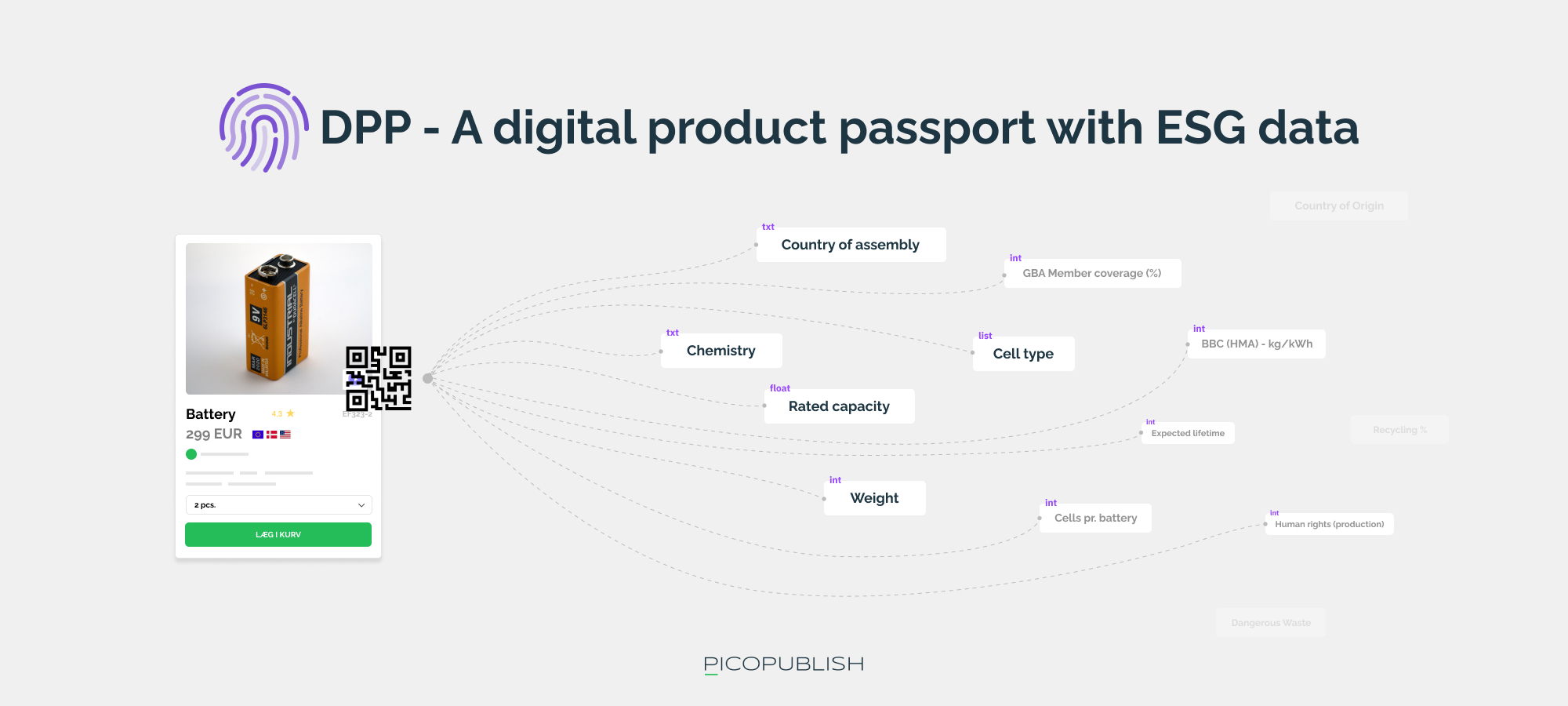

DPP - the idea of a Digital product passport is moving closer

Like the physical passport we are familiar with, the Digital Product Passport (DPP) serves as a document that accompanies a given product throughout its life cycle - from manufacturing to disposal.

The main purpose of the passport is to serve as a central source of information about the environmental properties of the product, including its recyclability.

At present, the digital product passport is still in the development phase. In 2022, an EU committee published a document entitled "On making sustainable products the norm", which refers to the digital product passport as follows:

"Digital product passports will become the standard for all products regulated under the ESPR, enabling products to be labelled, identified and linked with data relevant to their circularity and sustainability [...] Depending on the specific product, this may include information on energy consumption, recycled material, presence of substances of concern, durability, repairability including a repairability assessment, availability of spare parts and recyclability.

(Source: Europa.eu)

The requirement for documentation covers the entire life cycle of the product

Everything from the purchase of materials to recycling opportunities must of course be documented in the digital product passport.

Initially, access to the passport will be purely digital (e.g. via a QR code, an NFC chip, or an RFID tag).

The data collection therefore begins already in the design phase of the product, where it is documented:

- What materials the product contains

- Where the materials originate

- The place of production (in connection with freight/shipping)

The plan is for the digital passport to be continuously updated with details about sales, transport, or if the product has undergone repairs.

The concept of a Digital Product Passport is undoubtedly ambitious, and its success depends on the creation and maintenance of thousands of data points related to the production, logistics, service, and disposal of products or product parts.

Demo of a Digital Product Passport from the Global Battery Alliance

One of the industries that is first affected by sustainability requirements is the battery industry. For the same reason, the global association of battery manufacturers has created a proof of concept on a Digital Product Passport, which takes on the task of presenting data related to the sustainability profile of batteries.

This entire demo is digital, and can be seen here: https://www.globalbattery.org/action-platforms-menu/pilot-test/pilot-1/.

Read more about sustainability reporting

Are you ready for a non-binding chat?

Have you read what you needed, and are you ready to have a concrete conversation about challenges, needs, and solutions? Then feel free to contact us today.

Contact