The ESRS standard is your primary tool in the work with sustainability reporting

In the EU's new sustainability paradigm, reporting of ESG data will take up much more space than before.

Where the Double Materiality Analysis is your method (and is also mandatory in accordance with the CSRD directive), the ESRS standard is your tool.

In order to come to the rescue of companies that are, for example, affected by the requirements of the CSRD directive, the EU, with the help of the independent financial organization EFRAG, has prepared a standard for sustainability reporting called ESRS (European Sustainability Reporting Standard).

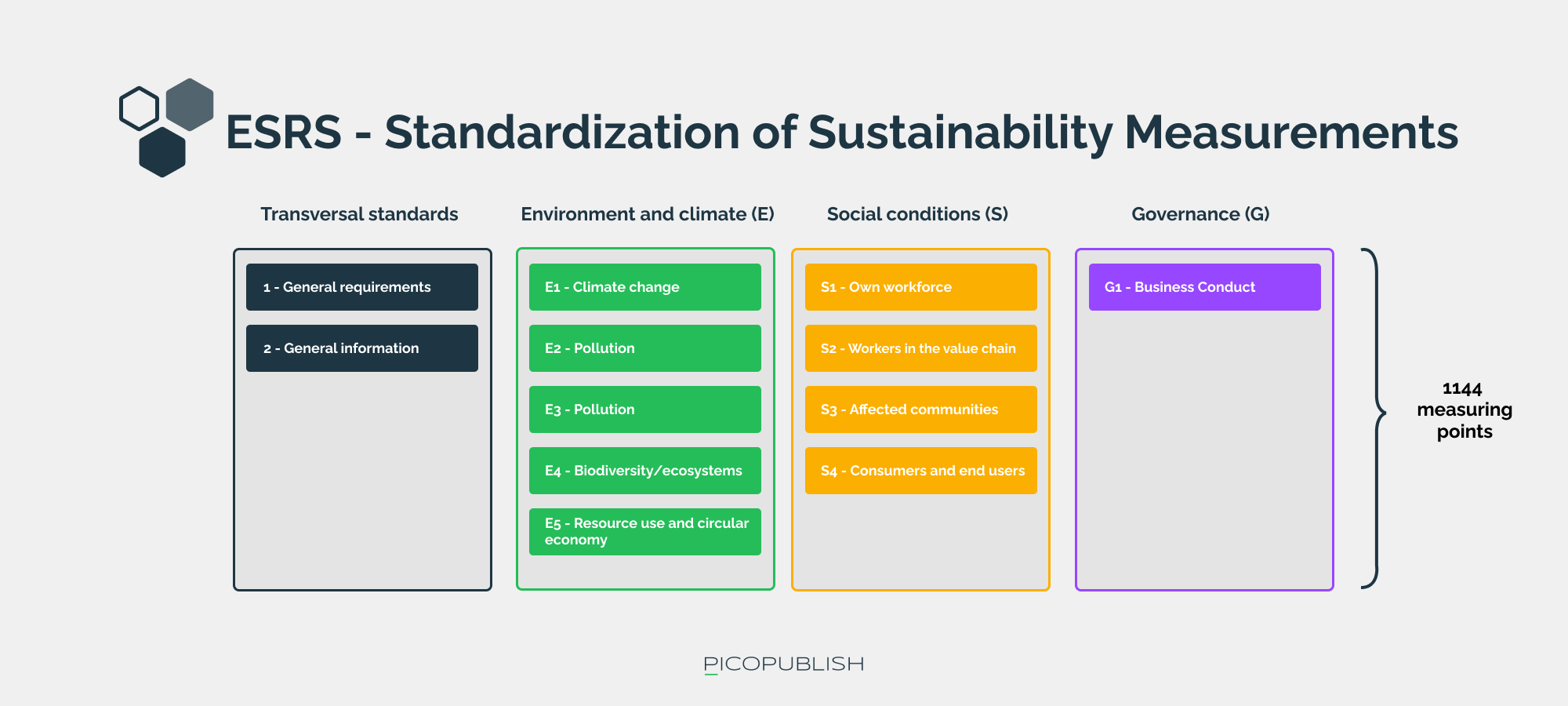

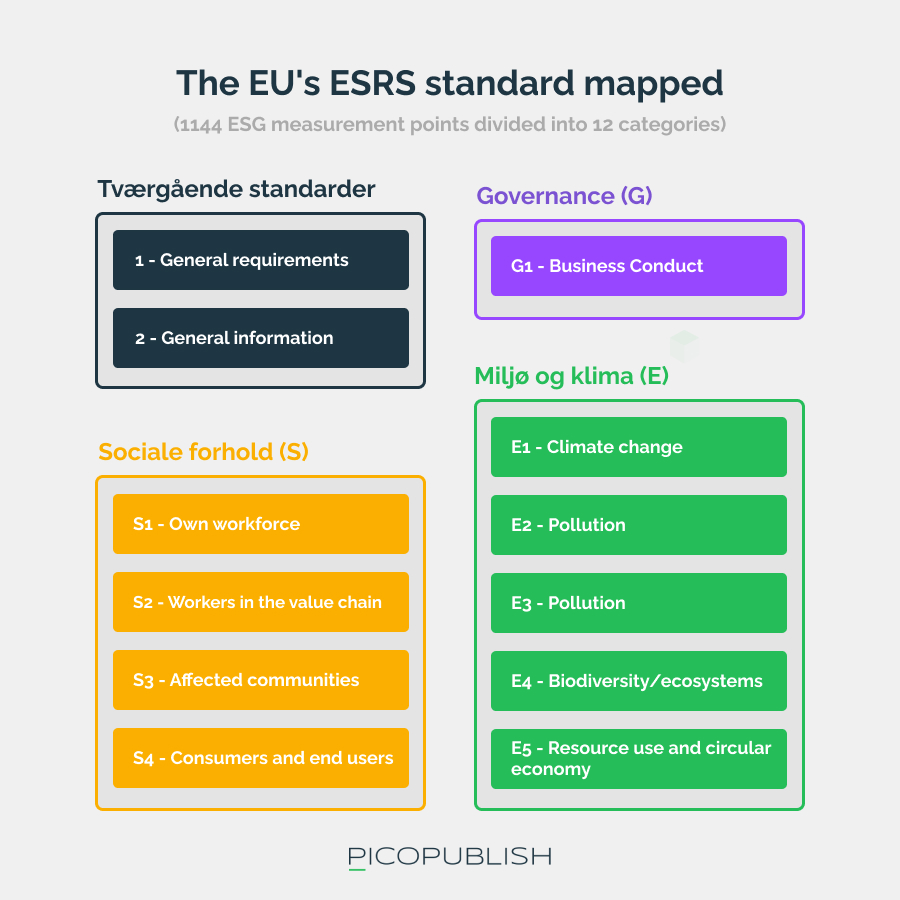

The standard maps in 12 categories the 1144 measurement points that companies must decide on when they begin their sustainability reporting in 2024.

The ESRS standard specifies across 12 categories which 1144 measurement points companies covered by the CSRD directive must report on.

What is the ESRS standard?

The ESRS standard is intended as a guide to reporting ESG data for companies covered by the CSRD Directive.

Initially, only companies with 500+ employees will be covered by the requirements. However, it is our expectation that these companies will require their smaller subcontractors and partners to provide ESG data in connection with the companies' trade.

The ESRS standard helps companies with their reporting by making visible;

- what the company should measure,

- how to measure

- what they must document in connection with the measurement.

The standard has been published in a preliminary format that is continuously updated and maintained. This is done based on the actual reporting companies make as a result of the CSRD directive's implementation in 2024.

Want to talk data?

If you’re interested in hearing our ideas on how data can help your business execute, grow, and scale, we’re ready for a no-obligation conversation.

Why is the ESRS standard relevant?

The ESRS standard contains the specific reporting requirements required by the CSRD Directive.

Because reporting ESG data is as extensive an undertaking as it is, it makes perfect practical sense to use the ESRS standard as a starting point when the company is getting started with its sustainability reporting.

In the first year of the ESRS standard, it will be possible to omit documentation/reporting in selected areas, as the standard is not considered to have been thoroughly worked out in these areas.

Other areas in the report may be omitted by companies that do not consider that the matter meets the requirements for double materiality.

ESRS - standardization of sustainability reporting

Much has been said about the green transition, which for many years has been a central topic in companies' CSR profiling. However, "exactly" is rarely a word associated with this discourse.

In recent years, concepts such as "greenwashing" have become an essential part of the debate. In 2022, a verdict was handed down in a case where a company was convicted of marketing PVC-enriched products as "environmentally friendly".

Sustainability standards and CSRD

To make sustainability reporting more accurate and quantifiable, the EU has developed the ESRS standard in collaboration with EFRAG, which forms the foundation for CSRD reporting.

EFRAG (European Financial Reporting Advisory Group) assists the EU in the development of legislation and standards for financial reporting. With ESRS (European Sustainability Reporting Standards), EFRAG has created a comprehensive reporting template consisting of 1144 points that serve as the basis for companies' CSRD reporting.

Reporting of "essential" parameters

Companies are required to carry out a double materiality assessment to determine the relevance of different social, environmental or societal factors for reporting. This double materiality principle ensures that companies consider both their impact on and their impact on ESG parameters.

In doing so, companies are encouraged to put themselves in an ethical and moral mirror when reporting on matters that affect staff, the environment, employment conditions and general trends in the local community.

The ESRS standard: a comprehensive reporting framework

The ESRS standard includes 12 categories:

- General principles

- General disclosures

- Climate Change

- Pollution

- Water & marine resources

- Biodiversity & ecosystems

- Resource use and circular economy

- Own workforce

- Workers in the value chain

- Affected communities

- Consumers and end-users

- Business conduct

These categories reflect the breadth of sustainability reporting. Both large and small companies need to prepare for the fact that data on these areas will soon become a crucial factor in their trade relations.

Companies with the necessary data become attractive trading partners, while those without data risk being excluded from supply chains where electronic data interchange (EDI) becomes a prerequisite for cooperation.

How does ESRS relate to other sustainability concepts?

ESRS (European Sustainability Reporting Standards) have been prepared by EFRAG, which is a private, EU-supported consultancy company that prepares guidelines for financial reporting in Europe.

How ESRS and CSRD are linked - the underlying reporting standard

In short, the CSRD report must be based on the ESRS standard. The ESRS standard contains 14 categories and 1144 measurement points that companies must consider to a greater or lesser extent when preparing their ESG reports.

How ESRS and DPP are connected - the underlying reporting standard

What DPP and ESRS have in common is that they are both tools for measuring and reporting ESG data.

The DPP concept is still so new that we do not yet know what requirements will be placed on the companies.

However, it is special for DPP that we are talking about product-related data. In this context, the PIM system stands out as an obvious candidate for collecting, organizing and publishing the necessary data. We have written an article about this here - "Why is the EU's upcoming "Digital Product Passport" interesting for PIM system owners?".

VSME – a "mini ESRS standard" for SMEs

VSME – a "mini ESRS standard" for SMEs

VSME stands for "Voluntary Reporting Standard for SMEs (VSME)" and is a simplified version of the EU's ESRS standards, which are primarily intended for companies with more than 500 employees or an annual turnover exceeding DKK 250 million.

The VSME standard is divided into two modules:

-

A basic module: Intended for micro-enterprises and serves as a minimum requirement for other companies.

-

A comprehensive module: Includes additional data points that are likely to be requested by banks, investors, and larger customers in addition to the basic information.

Data formats and reporting requirements

Companies are required to report data in specific formats to ensure consistency and comparability:

-

Energy and greenhouse gas emissions:

Energy consumption is reported in megawatt-hours (MWh), with a breakdown between fossil fuels and electricity. Greenhouse gas emissions are measured in tonnes of CO₂ equivalents (tCO₂eq) and divided into Scope 1 (direct emissions) and Scope 2 (indirect emissions from purchased energy). -

Pollution:

Information on emissions to air, water, and soil, including specific pollutants and quantities. -

Biodiversity:

Description of activities that impact biodiversity and any protection measures in place. -

Water consumption:

Total water usage in cubic meters (m³), including details on sources and any recycling efforts. -

Resource use and waste:

Quantities of materials used and waste produced, including recycling rates. -

Workforce:

Data on the number of employees, gender distribution, types of employment, occupational health and safety indicators such as accident frequency, as well as information on wages and training activities. -

Governance:

Information on any legal judgments or fines related to corruption and bribery, as well as gender diversity in leadership.

By following the VSME standard, small and medium-sized enterprises can structure their sustainability reporting in a way that meets stakeholders’ information needs and supports their own sustainable development.

You can read more about the VSME standard here:

https://www.efrag.org/en/projects/voluntary-reporting-standard-for-smes-vsme/concluded

Read more about sustainability reporting

Are you ready for a non-binding chat?

Have you read what you needed, and are you ready to have a concrete conversation about challenges, needs, and solutions? Then feel free to contact us today.

Contact