Learn more about what the ESG concept is for a size

The EU's new sustainability agenda focuses on reporting data related to social, environmental and corporate governance. The reporting will help to highlight how companies today contribute to a more sustainable society, and how they can do even more in the future.

ESG is simply a collective term for all data that falls into the categories "Environmental", "Social" or "Governance". In the EU's newly developed standard for measuring sustainability initiatives, ESRS, the more than 1144 measurement points covered are divided into categories that directly correspond to the ESG categorization.

ESG will most likely become a term that many companies will label their sustainability programs and projects with.

The ESG concept - why do we have to deal with it?

"ESG data" or "ESG reporting" is a basic classification in corporate reporting that covers three key areas:

Environmental (Environmental aspects)

Social (Social Conditions)

Governance (Business management and governance)

From 2024, these areas will be central to companies' reporting obligations, as the EU is currently rolling out a large number of directives and regulations that have been adopted by law.

Legal requirements for ESG reporting

With the implementation of directives such as the CSRD, it becomes mandatory for companies to report on ESG-related data. This emphasizes the necessity for companies to familiarize themselves with the latest legislation, requirements, and the tools available to facilitate sustainability reporting.

There is still uncertainty about how sustainability reporting will specifically affect Danish companies.

The expectation is that CSRD principles will be implemented in Danish legislation from 1 July 2024, while companies with more than 500 employees must comply with these reporting requirements as early as 1 January 2024.

Since companies with more than 500 employees are already subject to reporting requirements from 1 January 2024, several have criticised the introduction of legislation with retroactive effect. Therefore, it will also be interesting to follow the legal development, as sanctions, fines, etc. are currently unknown.

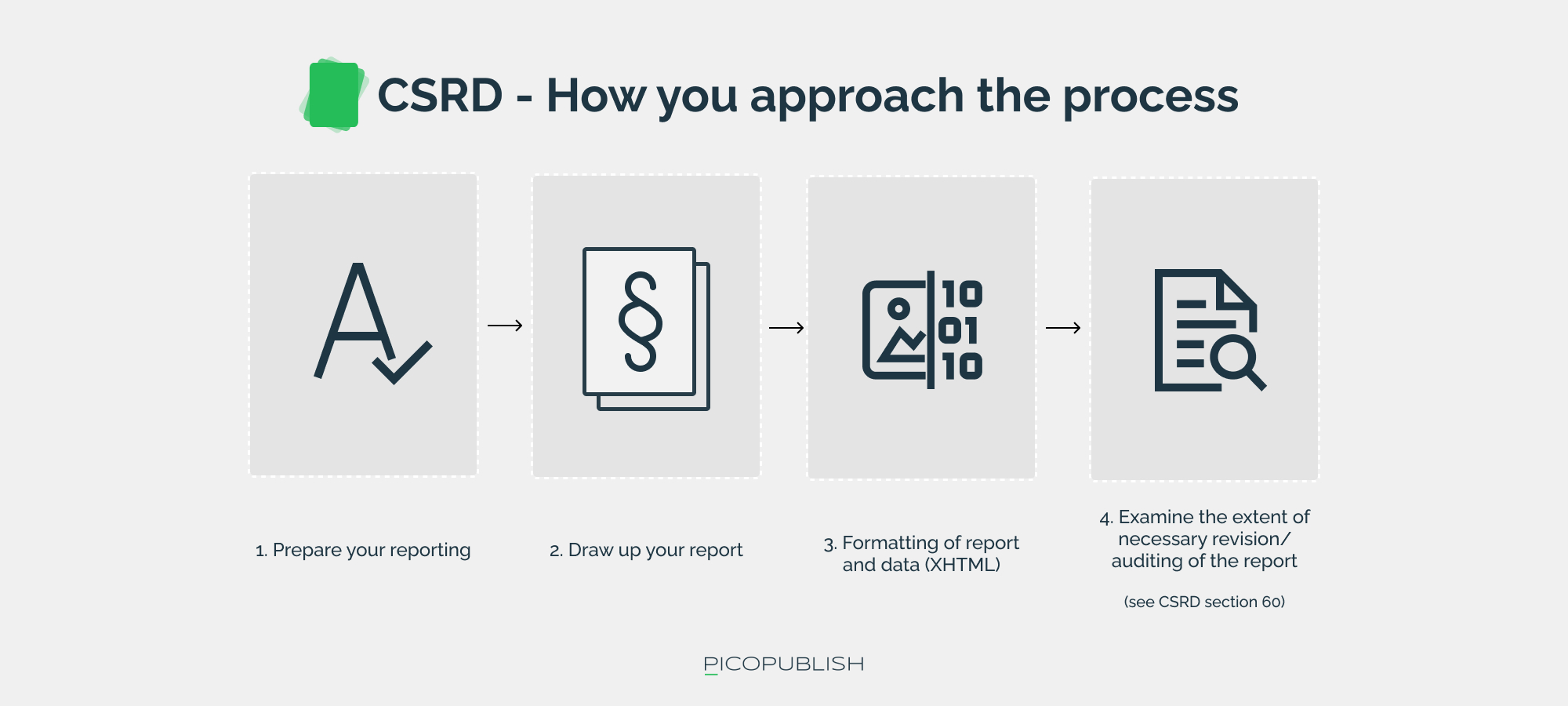

CSRD - Corporate Sustainability Reporting Directive (affects companies in 2024)

The CSRD (or "Corporate Sustainability Reporting Directive") is an EU directive that requires companies with more than 500 employees to report on their sustainability profile. The directive will be incorporated into Danish legislation during 2024.

Initially, the requirements for sustainability reporting in the CSRD Directive apply to companies in accounting class D with 500+ employees. However, smaller companies are indirectly affected by the requirements placed on the larger companies, where e.g. "CO2 emissions in the supply chain" becomes a measurement point.

Are you ready for a non-binding chat?

Have you read what you needed, and are you ready to have a concrete conversation about challenges, needs, and solutions? Then feel free to contact us today.

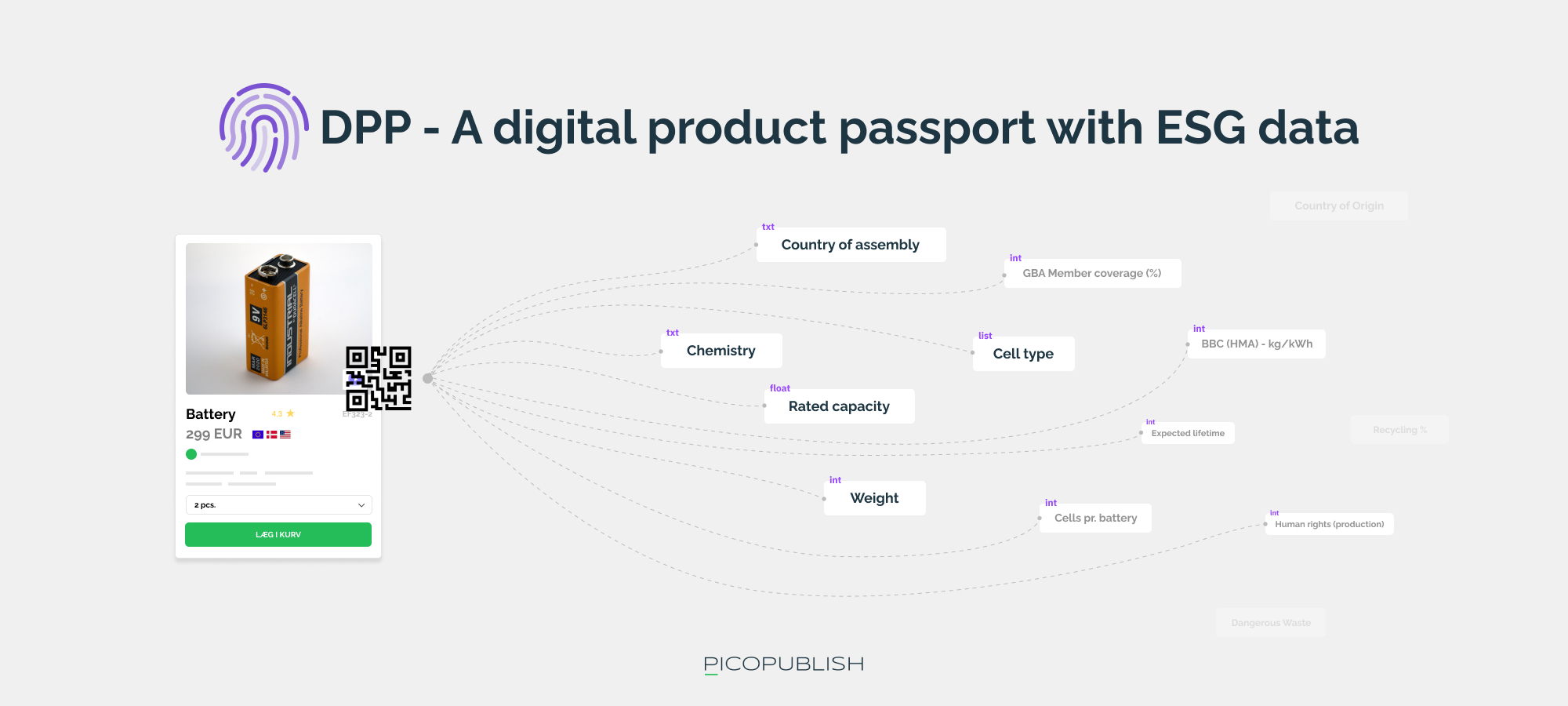

ContactDPP - A new digital product passport (implementation date unknown)

Just like the passport we know, the digital product passport is a document that must follow the product on its journey - from production to phase-out. The function of the passport is to be the primary source of information about the product's sustainability profile, including opportunities for recycling.

The digital product passport was born in and by the EU, and is currently still a theoretical construction that needs to mature, including through a number of "Call for proposals", where conditions related to format and scope must be clarified.

In 2022, an EU committee published the document "On making sustainable products the norm", in which the digital product passport is described:

"Digital product passports will be the norm for all products regulated under the ESPR, enabling products to be tagged, identified and linked to data relevant to their circularity and sustainability [...] Depending on the product concerned, this can include information on energy use, recycled content, presence of substances of concern, durability, reparability, including a reparability score, spare part availability and recyclability." (Source; Europa.eu)

Directives and regulations in the ESG category

The EU has set itself the ambitious goal of becoming a CO2-neutral continent by 2050. To support a green transition, the EU is preparing a number of legislative initiatives that address different aspects of sustainability and environmental protection.

Packaging and Packaging Waste Directive 94/62 (affecting businesses in 2024)

One of the directives that will enter into force as of 2024 is Directive 94/62/EF. The Directive affects the liability of companies in connection with the handling (e.g. production/disposal) of packaging.

A "directive" is EU legislation that needs to be adapted and transposed into the national law of each member state. This is in contrast to a "regulation" where the EU's words of praise are directly applicable.

With 92/64/EF, the EU hopes to:

- Reduce the amount of packaging waste

- Promote the reuse, recycling and recycling of packaging waste

In short, the EU wants a more circular economy, where all materials have a longer life cycle:

"By end of 2024, EU countries should ensure that producer responsibility schemes* are established for all packaging. Producer responsibility schemes provide for the financing or financing and organisation of the return and/or collection of used packaging and/or packaging waste and its channelling to the most appropriate waste management option, as well as for reuse or recycling of the collected packaging and packaging waste." (Source: EUR-LEX)"